Fixed income bonds

Fixed income and bonds are the world's biggest asset class. Understanding how they work will help you see how they can fit into your managed funds portfolio.

- Bonds are loans made by investors to governments or companies that need capital.

- The bond market is the world's biggest asset class.

- Before investing in a bond you should know who issued it, its credit quality and its duration.

- Managed funds make money from their bond portfolio through aggregate interest rate payments and changes in the capital values of the bonds in the portfolio.

Bonds and fixed income assets are the biggest investment asset class in the world. At an estimated $US226 trillion in 2020 as the world was hit by a global health crisis and global recession, this makes them around three times the size of world equity markets.

While bonds sound complicated, they are just loans - when you invest in bonds you are agreeing to lend money to someone who needs it, whether they are a government, a business or a consumer. But unlike normal loans

where most people go to their bank and ask to borrow money, with bonds the group that wants to borrow the money goes to the investment market to issue a contract, which is really just a request for how much they would like to borrow, the interest rate they are willing to pay and the term, that is, how long they want to pay off the loan. Often loans are auctioned, where the investors offering to receive, or accept, the lowest yield get to buy the bond on offer.

The interest rate, which makes up the yield on the investment, is called the coupon rate, and the term of the loan is referred to as its period until maturity.

In practical terms this means that when a government or a company issues a bond they are simply borrowing money, and when an investor such as a managed fund invests in that bond they are simply agreeing to lend

money according to the conditions of the bond. This is why bond markets are also called the debt markets.

The bond market is made up of several segments based on who issues the bond, its quality or level of risk and how long until it matures. Investors should be aware that their managers make money from bonds through both

the yield and changes in the bond's capital value.

Government bonds

The largest sector of the bond market by size are bonds issued by governments. For example, if the Australian government runs a budget deficit - meaning its annual taxation receipts are less than its annual income

- because it doesn't have that money in taxation receipts, it has to borrow it. While governments could just go to the bank to borrow the money, because they are so big it's cheaper for them to go directly to large-scale investors and get lower rates of interest than a bank would charge.

Investors like lending money to governments because governments, in theory, can just increase taxation rates if they need money (despite the risk that this can lead to a currency crisis). As a result, governments should never run out of money to repay their debts - this makes them low-risk borrowers and highly favoured by investors. And because governments are so often running up bigger and bigger debts it means there is never a shortage of governments issuing new bonds. This makes government bond markets highly liquid.

Governments being at very low risk of not repaying their bond debts is referred to as them having a very low chance of defaulting on this debt. But some governments have gone through periods where they have not been able to repay bond investors. Recent examples are Turkey in the 1970s, Russia in 1998, Argentina in 2001 and Greece in 2012. Even the US and UK have defaulted on their debts at certain points in their history.

While governments having huge debts is a problem, it's actually a bigger problem for the investors who loaned them the money because if the country's economy collapses the bond investors won't be paid. This means that even though the US is the world's biggest borrower, it's also crucial for everyone to help the US economy recover quickly and perform as strongly as possible.

Largest government bond markets June 2021

| Country | $A billion |

| United States | 34,277 |

| Japan | 13,919 |

| China | 10,859 |

| United Kingdom | 4,984 |

| France | 4,008 |

| Italy | 3,749 |

| Germany | 3,264 |

| Canada | 2,645 |

| Spain | 2,056 |

| Australia | 1,377 |

Source: Bank for International Settlements

Private sector bonds

The second largest sector is private sector bonds, referred to as corporate debt. Some large companies are bigger than countries in terms of their balance sheets and revenues, and they issue debt of the highest quality. For example, in the US, AT&T is known as the most indebted company in the world with outstanding bonds of around $US147 billion. The global corporate debt market is estimated to be worth around $US8 trillion, or $11 trillion in Australian dollars.

The corporate bond market in Australia, in contrast, is estimated at around $600 billion, meaning it's only about 60% the size of Australia's government bond market.

It may also surprise investors that Australian banks are very big borrowers in overseas bond markets. This is because they source only about two-thirds of all the money they lend to Australians from bank deposits, which forces them to borrow the shortfall overseas. Consequently, Australian banks are vulnerable to what happens to overseas bond markets and global interest rates.

Bond credit quality

When managed funds and other investors consider investing in a bond, that is, they are considering if they should lend money to a government or a company, it is important that they assess the quality of the bond. This is done by reviewing what are known as bond credit ratings. Bond credit ratings attempt to give investors an indication of the likelihood of a bond issuer honouring their debts - that is, they are trying to predict the likelihood that the bond may go into default.

There are dozens of bond credit rating agencies around the world, but the major ones are Standard & Poor's, Fitch Ratings, Moody's, China Lianhe Credit Rating, China Chengxin, Capital Intelligence Ratings, Veda (now part of Equifax), Japan Credit Rating and Dun & Bradstreet. Different agencies have specialities in global bonds, government bonds, corporate bonds, bonds issued in growth economies, such as Russia, China and India, or bonds issued for special projects, such as alternative energy.

In Australia we think of government debt as being the highest quality given that Australia has the highest possible AAA credit rating. But this isn't true across the world as credit quality varies greatly all the way across the bond market and within segments.

Within governments, too, there are variations. Treasury debt, that is, bonds issued by governments, is usually considered the highest quality, with other government agencies (right down to local government) offering bonds of varying quality. Government debt can be issued both in the currency of the country (called local currency debt) or in some other currency (usually US dollars but also euros and yen).

Other companies at the bottom of the quality spectrum issue bonds that investors call "junk". Investors will still lend money to low-quality companies if the interest rates they receive are high enough to justify the high default risk.

Bond rating grades

| Investment grade | Quality score |

| Aaa, AAA | Highest quality |

| Aa1, Aa2, Aa3, AA+, AA, AA- | High quality but some long-term default risk |

| A1, A2, A3, A+, A, A- | Medium quality but some negative concerns |

| Baa1, Baa2, Baa3, BBB+, BBB, BBB- | Medium quality but long-term warning signs |

| Non-investment grade | Quality score |

| Ba1, Ba2, Ba3, BB+, BB, BB- | Speculative fundamentals |

| B1, B2, B3, B+, B, B- | Invest with caution |

| Caa1, Caa2, Caa3, CCC+, CCC, CCC- | Poor quality, high default risk |

| Ca, CC | Low quality |

| C | Very low quality |

| D | In default |

Maturity

Bond maturity refers to how long until the bond, or the debt, is fully repaid. For example, if you think of your house mortgage as a bond you have issued to the bank, its maturity is most likely 30 years. Maturities can be as short as one day or as longas 30 years (such as the 30-year Treasuries offered by the US government), although the Argentinian government has issued 100-year bonds. The popularity of these ultra-long-term bonds is even generating interest in the US, which is considering whether it should also issue 50-year and 100-year bonds.

Some bonds are offered in perpetuity, meaning they never have to be repaid but the issuer promises to keep paying the coupon forever.

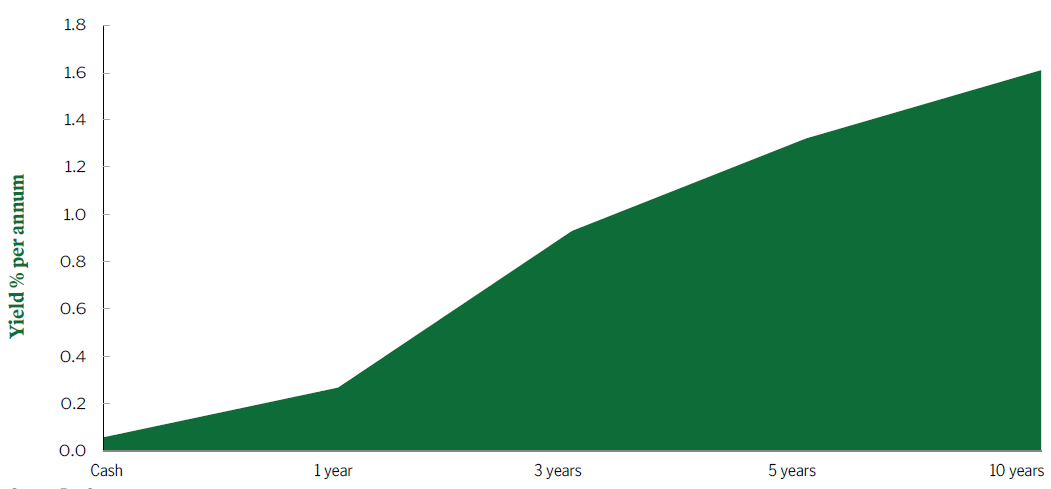

One way to assess the bonds market is to examine what is known as the yield curve, which is a chart of how average interest rates vary according to their maturity. The yield curve is very useful because it gives investors an indication of market sentiment towards future interest rate movements. For example, the yield curve for Australian interest rates shows that while over the short term investors are happy to invest in bonds paying about 0.1%pa, to invest over the longer term they want higher rates of almost 1.0% to justify longer-term risks, such as their expectations that interest rates will eventually go up and longterm inflation. For comparison, investors in 100-year Argentinian bonds have been promised 8% yields.

How your managed fund makes money investing in bonds

When a bond issuer issues a bond for, say, $10 million with a five-year maturity paying a 3% interest rate yield, the bond by definition is worth $10 million because that is what the investor (the managed fund) paid for it, that is, loaned the issuer. But let's say the managed fund's investment manager believes inflation is about to increase from 2% to 3%, meaning the 3% yield is no longer 1% above inflation but just matching it. The investment manager will probably want to sell the bond and buy one paying a higher interest rate, perhaps 4%.

To achieve this the investment manager has to sell the bond, possibly for a loss. But the investor they sell the bond to will still receive the yield of 3% on the face value of the bond, being an interest coupon payment of $300,000 pa on the $10 million bond certificate. But if the new owner of the bond buys the bond for, say, $7.5 million, then the $300,000 interest yield payment would convert to an effective yield of 4%. So the first investor has suffered a 25% investment loss to get the poorly performing bond out if its portfolio only to see the new owner of the bond receiving an effective 4% yield.

This example illustrates how the prices of bonds, generally speaking, move in the opposite direction of yields (the effective interest rate). Put another way, when interest rates go up, bond prices fall, and when interest rates go down, bond prices go up.

If your managed fund is good at analysing and forecasting which way interest rates will shift, it is easy to see how it can make money for the fund - and for an investor in that fund.

There are also some basic mechanics around bond investments of which investors into managed funds that have a high emphasis on bonds should be aware. For example, when a bond is issued it has a fixed coupon that is paid every six or 12 months. The coupon amount is based on interest rates at the time of issue. The price of the bond is based on all the future cashflows coming from that bond, including the return of capital when the bond matures. If interest rates subsequently rise, future bonds will reflect those changes in the coupon paid.

As a result, the price of any existing bonds must fall so that the total return (coupons plus the return of capital or face value) to maturity is the same. The opposite happens when interest rates fall. The price of existing bonds rise so that anyone buying that bond will get the same return as someone buying a new bond with the same maturity.

However, long-maturity bond prices are more sensitive to interest rate changes than short-duration bonds because they have more cashflows in the form of future interest rate coupon payments compared with short-duration bonds. The price has to change more to compensate for this fact. This is known as interest rate risk.

Australian government bond yield curve - December 2021

Source: FactSet

| Capital return | + | interest payment | = | your bond's investment return |

| When you invest in a managed fund bond portfolio you make money in two ways: from the interest rate payments and the capital return, that is, the increasing capital value of the bonds in the portfolio. This makes bond investments more sophisticated than bank term deposits, which only pay you an interest rate. | ||||

| Property |

| Cash |